“Everything you need to know about Conventional Loans”- FTHB Series

Now that we have identified all of the different mortgage options and their general differences, we will start breaking down each option in more detail. In this post we will be covering “Everything you need to know about Conventional Loans”. If you missed our last post, Click Here to check it out.

Mortgages can fall in one of two categories. They can be defined as either government-backed or conventional. Government agencies like the Federal Housing Administration (FHA) and the Department of Veterans Affairs (VA) insure home loans, which are made by private lenders. This insurance is paid for by fees collected from mortgage borrowers and protects lenders from default. The US Department of Agriculture (USDA) loans money to lower-income borrowers through its Direct Housing Program. It also guarantees loans made by private lenders through its Guaranteed Housing Loans program. This backing is paid for by borrowers.

Mortgages not guaranteed or insured by these agencies are known as conventional home loans. They include:

- Conforming loans

- Non-conforming loans

- Jumbo loans

- Portfolio loans

- Sub-prime loans

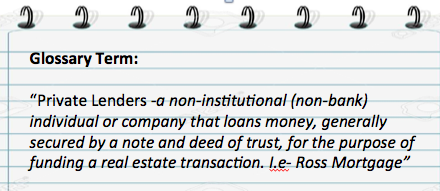

For these mortgages that are not guaranteed or insured by a federal agency, lenders get assurance through a down payment of at least 20% or more. However, a down payment of 20% is not necessarily required for the buyer to get approval on the loan. In these cases lenders will require Private Mortgage Insurance (PMI) to secure the loan.

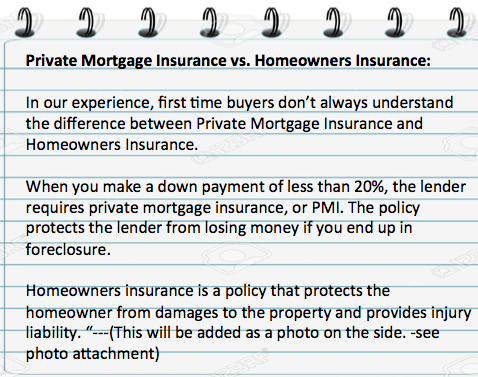

Private Mortgage Insurance vs. Homeowners Insurance:

In our experience, first time buyers don’t always understand the difference between Private Mortgage Insurance and Homeowners Insurance.

When you make a down payment of less than 20%, the lender requires private mortgage insurance, or PMI. The policy protects the lender from losing money if you end up in foreclosure.

Homeowners insurance is a policy that protects the homeowner from damages to the property and provides injury liability. “—(This will be added as a photo on the side. -see photo attachment)

About half of all conventional loans are called “conforming” mortgages, because they conform to guidelines established by Fannie Mae and Freddie Mac. These two government-sponsored enterprises (GSEs) buy mortgages from lenders and sell them to investors. Their purpose is to make mortgages more widely available. All conforming mortgages are also conventional mortgages.

Loans that do not conform to GSE guidelines are referred to as “non-conforming” home loans. Non-conforming loans that are larger than loan limits set by the GSEs are often referred to as “jumbo” mortgages. All non-conforming mortgages are also conventional mortgages.

Conventional loans held by mortgage lenders on their own books are called “portfolio” loans. Because lenders can set their own guidelines for these loans and do not sell them to investors, these products may have features that other mortgages do not. For example, a portfolio lender might allow a borrower to use investments like stocks and bonds as security for a mortgage for which she would not otherwise qualify.

Conventional home loans marketed to borrowers with low credit scores are called sub-prime mortgages. They typically come with high interest rates and fees. The government has created special rules covering the sale of such products, but they are not government-backed — they are conventional loans.

Who they’re for: Conventional mortgages are ideal for borrowers with good or excellent credit.

How they work: Conventional mortgages are “plain vanilla” home loans. They follow fairly conservative guidelines for:

- Borrower credit scores.

- Minimum down payments.

- Debt-to-income ratios.

Cost: Closing costs, down payments, mortgage insurance and points can mean the borrower has to show up at closing with a sizable sum of money out of pocket.

What’s good: Typically, conventional mortgages pose fewer obstacles than Federal Housing Administration or Veterans Affairs mortgages, which may take longer to process.

What’s not as good: You’ll need excellent credit to qualify for the best interest rates.

Are you looking to buy a house and need a mortgage? We would love to help! Please leave a comment or Click Here and find the most convenient way for you to contact us.

Submit a comment